Albert Lopez

Global head of BSO, Regional Managing Director (Americas), BDO Global

In exploring the role of the CVO and how the role of the CFO is developing ACCA and BDO consulted nearly 100 finance leaders from across many geographies. There are two key questions:

There is no uniform definition of value. Indeed, one CFO commented that ‘value is in the eye of the beholder’. The nature of value in respect of an organisation will depend upon its location, its sector and its size.

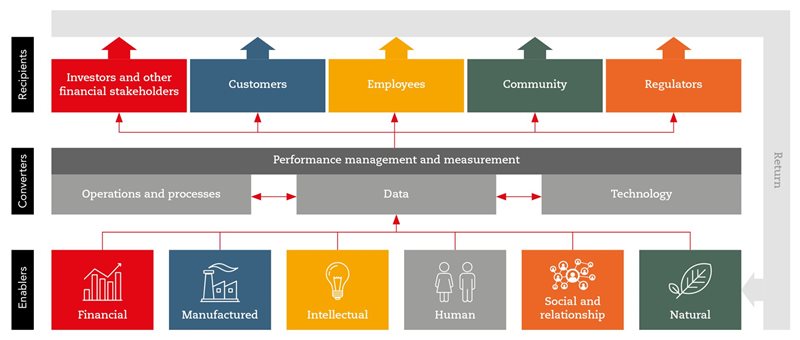

Figure 1 illustrates the processes by which organisations enable and convert value for the benefit of its recipients, the stakeholders in the organisation.

Value is enabled by the interaction of several elements of an organisation which can be represented in the Integrated Reporting Framework of the International Integrated Reporting Council (IIRC). It is the combination of these capitals which delivers the value. For several CFOs who participated in the research it is the human capital in its interaction with the others that creates the value by creating the synergies necessary to deliver the value.

These enablers operate through a series of processes which in turn create data both of which activities are increasingly supported by technology. Once more it is the human intervention that takes the data and analyses and interprets it in a way that facilitates the management and measurement of performance. In a value centric organisation these performance measures are not solely financial in nature. Indeed, several CFOs spoke of utilising metrics such as net promoter scores as part of their customer data to assess the extent to which value was being created by the organisation for its customers.

These customers are one example of the range of the recipients of value. Organisations have been traditionally very profit focused for the benefit of investors and other financial stakeholders. Increasingly as organisations turn to consider their long-term sustainability that range of stakeholders has broadened to include customers, employees, communities and regulators. Without creating the sustainable organisation as a combination of economic, environmental and social equity, the value of an organisation can diminish and hence there is a very strong causal link between value creation and strategy.

Value is cyclical. The actions of the recipients return value to the enablers and so the process continues.

FIGURE 1: A model of value Enablers Converters Recipients

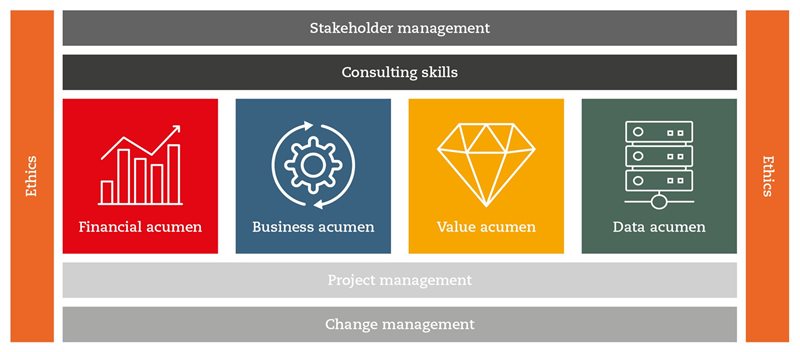

The CFO role continues to evolve. It is no longer just the scorekeeper for the organisation rather it is one of a strategic advisor who works closely with the chief executive officer to deliver on the goals of the organisation and to create value for its stakeholders. As such it is a role that looks to a broader view of performance but at its core retains a strong technical and ethical backbone which facilitates trust. The breadth of the role is illustrated by Figure 2

FIGURE 2: The reality of the CFO role

With the stewardship of the assets of the organisation the CFO is very much acting as a chief value officer. Many of the CFOs who contributed to the research saw their role as fundamental to the organisation. A role which required a comprehensive skill set both of technical and interpersonal skills. Rather than creating a new C-level role concerned with value, many CFOs felt that they were already delivering upon it.

The challenge for the finance team is to develop and maintain the relevant skill sets. To negate the impression that it is a function focused on historic performance rather than highlighting future opportunities. A function that is comfortable with both financial and non-financial data and views performance in a comprehensive manner. The reality is for most organisations that the CFO is the CVO.

Copyright © 2023 by the Association of Chartered Certified Accountants (ACCA). All rights reserved. Used with permission of ACCA. Contact insights@accaglobal.com for permission to reproduce, store or transmit, or to make other similar uses of this document.

Complete the form below to receive your copy of the full research report.

Albert Lopez